Strong AI and cloud momentum drives record licensing and royalty revenue; Armv9 adoption accelerates across hyperscalers

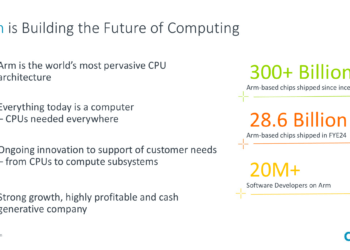

Arm reported a record-breaking fourth quarter of its fiscal year 2025, with total revenue climbing 34% year-over-year to $1.24 billion—its first quarter exceeding $1 billion. Royalty revenue reached an all-time high of $607 million, while license and other revenue surged 53% to $634 million, propelled by demand for high-performance custom silicon, Armv9-based architectures, and increased deployments in data centers. Full-year revenue rose 24% to $4.01 billion, with royalty income exceeding $2.1 billion for the first time.

The company emphasized its expanding footprint in AI infrastructure, noting that approximately 50% of new server chips shipped to top hyperscalers in 2025 are expected to be Arm-based. Notable customer momentum includes NVIDIA’s Armv9-based Grace Blackwell CPU in full production, Google Cloud’s Axion deployed in 10 regions and adopted by Spotify, and Microsoft Azure’s Cobalt 100 chips running key workloads from Databricks and Snowflake. Arm’s Compute Subsystems (CSS) and Flexible Access models are accelerating time-to-market and enabling broader cloud-to-edge AI compute adoption.

Key Q4 FY25 Highlights:

- Total revenue: $1.24 billion (up 34% Y/Y)

- Royalty revenue: $607 million (up 18% Y/Y), driven by strong adoption of Armv9 CPUs and CSS-based SoCs

- License and other revenue: $634 million (up 53% Y/Y), fueled by multi-year licensing agreements and backlogged revenue

- Non-GAAP operating income: $655 million; non-GAAP operating margin: 52.8%

- Non-GAAP diluted EPS: $0.55 (up 53% Y/Y)

- Operating cash flow: $258 million; Free cash flow: $163 million

- Annualized Contract Value (ACV) grew 15% Y/Y to $1.37 billion

- Remaining Performance Obligations (RPO): $2.23 billion, with 25% expected to be recognized as revenue within 12 months

- Arm CSS entered new markets including automotive with a leading global EV OEM

- GAAP gross margin: 97.7%; Non-GAAP gross margin: 98.4%

Industry Trends Observed During the Quarter:

- AI data center demand is accelerating across hyperscalers, with NVIDIA, AWS, Google Cloud, and Microsoft integrating Armv9 chips into production systems

- Custom silicon demand is rising as enterprises prioritize energy efficiency, accelerated AI performance, and differentiated infrastructure

- Google’s Arm-based Axion chip showed strong uptake, now deployed in 10 regions and used by 40 of its top 100 customers

- Microsoft expanded Arm support to large-scale workloads across Azure (e.g., Databricks, Siemens, Snowflake, Microsoft Teams, Copilot)

- NVIDIA’s DGX Spark AI desktop, built on Grace Blackwell, highlighted adoption of Arm CPUs in edge AI infrastructure

- Arm’s Ethos-U85 NPU and Cortex-A320 CPU combined to deliver edge AI solutions supporting billion-parameter models for industrial and vision use cases

- Smartphone royalties grew ~30% Y/Y despite low-single-digit market volume growth, showing Arm’s increasing royalty per chip

- Arm launched a GitHub Copilot extension to help developers write more performant code optimized for Arm architectures

- Kleidi AI software layer now supports 8 billion+ cumulative installs across Arm-based devices

- Data center TCO benefits of Arm include improved energy efficiency, reduced thermal envelope, and lower price-performance ratios in production workloads

“AI growth from the cloud to the edge is creating demand for more energy-efficient compute,” said Arm CEO Rene Haas. “Arm will enable AI everywhere, and our record results reflect the accelerating adoption of our architecture across a broad range of next-generation infrastructure.”