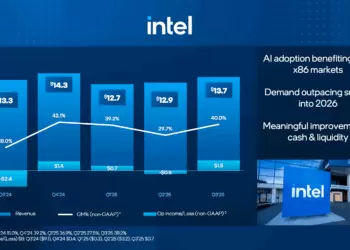

Intel reported $12.9 billion in revenue for the second quarter of 2025, flat compared to a year ago, while absorbing steep losses from restructuring and impairment charges. The company posted a GAAP loss per share of $(0.67), impacted by $1.9 billion in restructuring costs and $1 billion in impairment-related items. Non-GAAP EPS came in at $(0.10). Intel reaffirmed its ongoing cost-reduction efforts, with plans to reduce non-GAAP operating expenses to $17 billion in 2025 and $16 billion in 2026, and to hold gross capital expenditures to $18 billion this year.

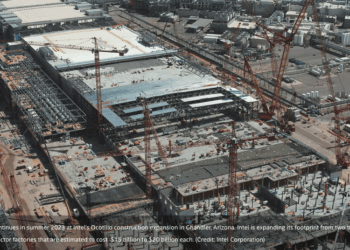

Intel is significantly restructuring its global footprint, halting expansion projects in Germany and Poland, consolidating assembly and test facilities from Costa Rica to Asia, and slowing development at its Ohio fab site. The company also cut roughly 15% of its core workforce, aiming to end the year with about 75,000 employees. Despite these cuts, Intel continues to invest in its foundry and AI businesses. Its Data Center and AI segment rose 4% year-over-year to $3.9 billion, while its Intel Foundry revenue increased 3% to $4.4 billion.

On the product side, Intel added three new chips to its Xeon 6 lineup, including the Xeon 6776P powering NVIDIA’s DGX B300 systems. The first Panther Lake CPUs remain on track for shipment by the end of 2025. Intel also confirmed that its advanced 18A process node has entered production in Arizona. For Q3 2025, Intel expects revenue in the range of $12.6–13.6 billion and flat non-GAAP earnings.

- Q2 2025 revenue: $12.9B (flat YoY)

- GAAP EPS: $(0.67); non-GAAP EPS: $(0.10)

- Restructuring and impairment charges: $2.9B combined impact

- Core headcount reduced ~15%; targeting 75,000 employees

- DCAI revenue: $3.9B (+4% YoY); CCG revenue: $7.9B (–3% YoY)

- Intel Foundry revenue: $4.4B (+3% YoY)

- Intel 18A entered production; Panther Lake CPU shipping on track

- Q3 2025 non-GAAP EPS guidance: $0.00 on revenue of $12.6–13.6B

“Our operating performance demonstrates the initial progress we are making to improve our execution and drive greater efficiency,” said Intel CEO Lip-Bu Tan. “We are laser-focused on strengthening our core product portfolio and our AI roadmap to better serve customers.”

Some key points from the investor call:

- Organizational Restructuring: Completed reviews of all org units; reduced management layers by 50%; on track for 75,000 employees by year-end; return-to-office set for September.

- Capital Discipline & Foundry Strategy:

- Ending fab projects in Germany and Poland.

- Slowing pace of construction in Ohio.

- Consolidating Costa Rica assembly/test ops into Malaysia and Vietnam.

- Capacity expansion will only occur with committed volume; no more “build it and they will come” mindset.

- Process Tech Update:

- Intel 18A: Ramp continues; foundation for next 3 generations of client/server products.

- Intel 14A: Early-stage design with outside customer input; CapEx only after performance and volume milestones.

- Product Focus:

- Client: Panther Lake SKUs to launch end of 2025; Nova Lake expected end of 2026.

- Server: Granite Rapids ramping; working to regain share in hyperscale with Diamond Rapids (~2026).

- Mandating CEO-level review of all major chip designs before tape-out.

- AI Strategy:

- Shifting focus to full-stack AI solutions with emphasis on inference and agentic AI.

- Building out x86 + Xe GPU foundation while adding software talent and targeting emerging workloads.

- Exploring purpose-built ASIC collaborations.

🌐 Why it Matters: Intel’s transformation into a competitive foundry player is capital intensive and will take time. The restructuring reflects a more disciplined approach to capital allocation and cost control. Success will depend on its ability to execute on roadmap milestones like 18A and build momentum in AI and foundry services.

🌐 We’re tracking the latest developments in networking silicon. Follow our ongoing coverage at: https://convergedigest.com/category/semiconductors/