Keysight ended fiscal year 2025 with fourth-quarter revenue of $1.42 billion, up 10% from a year earlier, driven by strong performance in commercial communications, aerospace and defense, and semiconductor test. GAAP net income reached $229 million, reversing a GAAP net loss of $73 million in Q4 2024, while non-GAAP EPS increased to $1.91, up 16% year-over-year. Orders grew 14% in the quarter, bringing the company’s FY25 backlog to $2.7 billion, positioning Keysight for a strong start to FY26.

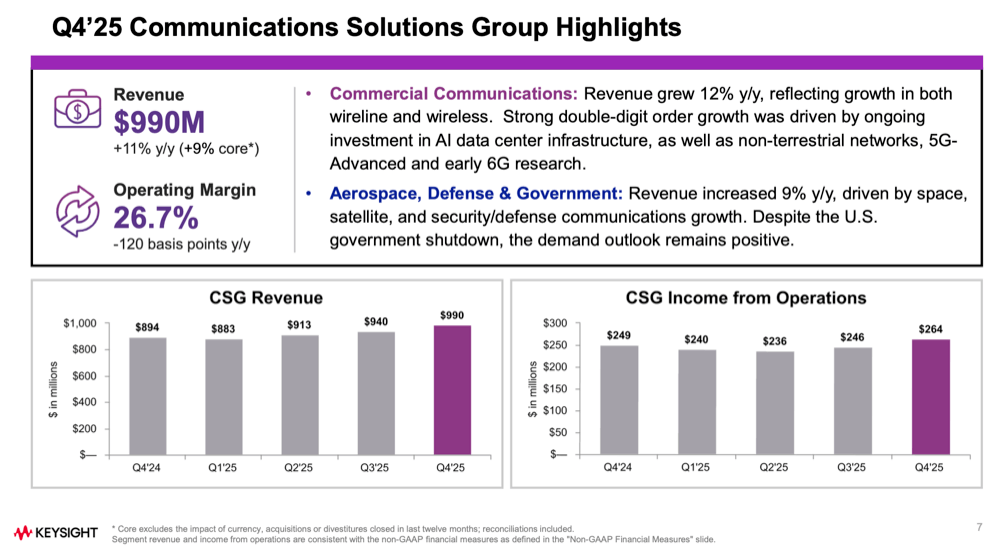

For the full fiscal year, Keysight posted $5.37 billion in revenue (+8% YoY) and generated $1.28 billion in free cash flow. The Communications Solutions Group (CSG) delivered $990 million in Q4 revenue (up 11% YoY), aided by investments in AI data center networking, non-terrestrial networks, and early 6G research. The Electronic Industrial Solutions Group (EISG) grew 9% YoY to $429 million, with strength in semiconductor wafer test, industrial electronics, and digital health systems.

Keysight also announced a new $1.5 billion share repurchase authorization. For Q1 FY26, the company guided revenue of $1.53–$1.55 billion and non-GAAP EPS of $1.95–$2.01.

Key Points

- Q4 revenue: $1.42B, up 10% YoY; FY25 revenue: $5.37B, up 8%.

- Non-GAAP Q4 EPS: $1.91, up 16% YoY.

- Q4 orders: $1.53B, up 14% YoY and 14% sequentially.

- CSG Q4 revenue: $990M, driven by AI data center, wireless, NTN, and 6G research.

- EISG Q4 revenue: $429M, with double-digit semiconductor test growth.

- FY25 free cash flow: $1.28B.

- New $1.5B share repurchase program authorized.

- FY25 acquisitions—including Spirent—expanded software-centric solutions and increased software mix by ~300 bps (see page 3) .

“Keysight delivered an outstanding quarter and strong close to the fiscal year, returning the company to full-year growth with order momentum accelerating through the year,” said Satish Dhanasekaran, Keysight’s President and CEO.

🌐 Analysis

The headline development this quarter is Keysight’s integration of Spirent, the network testing and assurance company whose acquisition formally closed earlier this month. The Q4 results presentation emphasizes Spirent as one of the three strategic FY25 acquisitions that expand Keysight’s software-centric portfolio and increase its addressable market by approximately $1.25 billion (see page 3) . Spirent brings long-standing strengths in 5G/6G core validation, cybersecurity test, GNSS simulation, and cloud-native assurance—directly complementing Keysight’s RF, wireless, and transport-layer test platforms.

With the transaction now closed, Keysight moves into a new competitive phase. Its combined assets with Spirent create a more vertically integrated test-and-assurance stack spanning physical, virtual, and cloud networks. This is particularly well-timed for customers deploying AI data center fabrics, disaggregated 5G/6G cores, and hybrid space–terrestrial architectures. Competitors in the test-and-measurement sector—Viavi (which recently closed its acquisition of Spirent competitor Spirent’s rival Spirent?)* and Rohde & Schwarz—will need to respond to the expanded breadth of Keysight’s software and automation capabilities. Near-term integration execution will be a key factor, but the strategic logic is clear: Spirent strengthens the software-led model that Keysight has been building toward for several years.