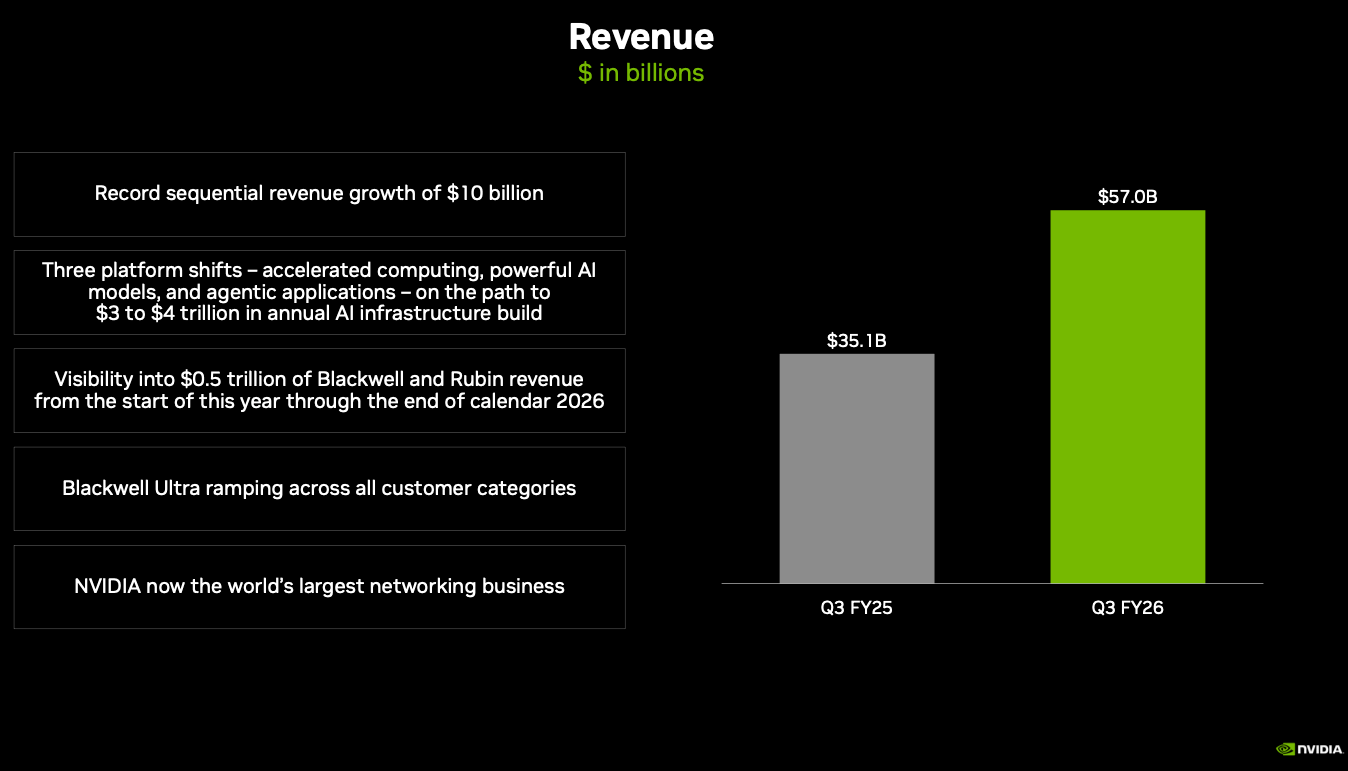

NVIDIA reported Q3 FY26 revenue of $57.0 billion, up 22% sequentially and 62% year over year, driven by sustained demand for AI compute and networking. Data Center revenue surged to a record $51.2 billion, reflecting the global build-out of GPU-powered AI factories, hyperscale inference clusters, and next-generation supercomputers. Gross margins reached 73.4% GAAP even as the company ramped Blackwell at scale, transitioning from component shipments to full-stack data center systems.

The company cited “off-the-charts” Blackwell demand and said cloud GPUs remain sold out across training and inference markets. NVIDIA highlighted the rapid shift toward massive-context foundation model training, agentic AI applications, and sovereign AI infrastructure. According to the Q3 investor presentation, NVIDIA now has visibility into $0.5 trillion of cumulative Blackwell and Rubin revenue through the end of 2026, underscoring unprecedented infrastructure investment across hyperscalers, nations, and industrial verticals.

In Q3, NVIDIA released a broad set of AI platform updates, including the Rubin CPX GPU for large-context workloads, NVQLink for hybrid GPU–quantum systems, and multiple large-scale projects with OpenAI, Anthropic, Microsoft, Oracle, and Google Cloud. The company also expanded its networking portfolio, noting in its presentation that NVIDIA is now “the world’s largest networking business,” with Spectrum-X and BlueField-4 positioned as core technologies for multi-gigawatt AI factories.

Explosive scale-out of GPU compute

- Blackwell adoption accelerating across hyperscalers and AI labs.

- OpenAI to deploy at least 10 GW of NVIDIA systems for next-generation training clusters.

- Anthropic adopting 1 GW of Grace-Blackwell and Vera Rubin systems for model scaling.

- Seven new supercomputers advancing, including DOE’s Solstice with 100,000 Blackwell GPUs.

Networking becomes a strategic bottleneck

- NVIDIA reports it is now the world’s largest networking vendor.

- Spectrum-X adopted by Meta, Microsoft, and Oracle for AI data center fabrics.

- NVLink and NVQLink push hybrid compute architectures—GPU-GPU and GPU-quantum.

AI factories enter industrial, telecom, and sovereign segments

- NVIDIA Omniverse DSX released as a blueprint for gigawatt-scale AI factory design.

- Collaboration with Nokia expands AI-RAN offerings for 5G-Advanced and early 6G RAN.

- Partnerships announced with governments in the U.K. and South Korea for national-scale GPU infrastructure deployments.

U.S. semiconductor reshoring milestone

- First Blackwell wafer produced at TSMC’s Arizona fab, marking U.S. manufacturing in volume.

Emergence of physical AI and robotics

- New DRIVE AGX Hyperion 10 platform for Level-4 autonomous fleets.

- IGX Thor introduced as a real-time industrial AI platform.

- Partnerships with Amazon Robotics, Foxconn, Caterpillar, Toyota, TSMC, and others.

Segment highlights

Data Center

- $51.2B revenue, +25% Q/Q, +66% Y/Y.

- Blackwell Ultra delivers 10× throughput per megawatt versus prior generation.

- NVIDIA investing across compute, networking, and quantum-hybrid architectures.

Gaming and AI PC

- $4.3B revenue, flat Q/Q, +30% Y/Y.

- DLSS 4 adoption expands with major AAA titles.

- TensorRT-optimized AI tools gain traction on RTX AI PCs.

Professional Visualization

- $760M revenue, +26% Q/Q.

- DGX Spark ships, delivering a compact AI supercomputer.

Automotive and Robotics

- $592M revenue, +32% Y/Y.

- NVIDIA and Uber target a 100,000-vehicle Level-4 mobility network.

- IGX Thor pushes real-time “physical AI” to factories and logistics operations.

“Blackwell sales are off the charts, and cloud GPUs are sold out,” said Jensen Huang, founder and CEO of NVIDIA. “Compute demand keeps accelerating and compounding across training and inference — each growing exponentially.”

🌐 Analysis

NVIDIA’s results confirm that the global AI infrastructure cycle continues to expand at extraordinary speed, with hyperscalers, model-builders, and sovereign programs all driving multi-gigawatt demand. The company’s increasing mix of full-stack data center platforms—compute, networking, software, and emerging quantum-coupled architectures—positions it as the central supplier for the next phase of AI factories. Competitively, AMD and Intel continue to ramp their AI portfolios, but the scale of NVIDIA deployments with OpenAI, Microsoft, Google Cloud, Oracle, CoreWeave, and multiple national governments places NVIDIA firmly at the center of 2026–2028 infrastructure buildouts.