On September 9, 2025 Synopsys posted third-quarter fiscal 2025 revenue of $1.74 billion, up 14% from $1.53 billion a year earlier. The results include contributions from Ansys, which Synopsys acquired on July 17. GAAP net income fell to $242.5 million ($1.50 per diluted share) from $425.9 million ($2.73 per share) in the prior year, while non-GAAP net income came in at $548.9 million ($3.39 per share) compared to $535.5 million ($3.43 per share) in Q3 2024.

CEO Sassine Ghazi called the quarter “transformational,” citing the Ansys integration and long-term opportunities in AI-driven product design, while noting that Design IP performance lagged expectations. CFO Shelagh Glaser added that Design Automation showed strength, but IP softness led to a more conservative Q4 outlook. Synopsys expects full-year revenue between $7.03 billion and $7.06 billion, with non-GAAP EPS in the $12.76–$12.80 range.

The company now reports results in two segments:

- Design Automation – includes silicon design, verification, Ansys simulation and analysis, system integration tools, and manufacturing software.

- Design IP – includes interface, foundation, security, and embedded processor IP, subsystems, and services.

Synopsys exited the software integrity business in 2024, with current financials reflecting continuing operations only. The company guided Q4 revenue between $2.23 billion and $2.26 billion, GAAP EPS between -$0.27 and -$0.16, and non-GAAP EPS between $2.76 and $2.80. Free cash flow for FY2025 is expected at ~$950 million.

“Q3 was a transformational quarter. Against a challenging geo-political backdrop, we closed the Ansys acquisition – expanding our portfolio, customer base and opportunity,” said Sassine Ghazi, president and CEO of Synopsys.

Key Points from Q3 2025 Investor Call

- IP Weakness Drivers – Three factors hurt Design IP: (1) new U.S. export restrictions disrupting design starts in China, (2) challenges at a major foundry customer delaying expected IP revenue, and (3) internal resource allocation decisions that slowed certain roadmaps.

- Pivoting IP Business Model – Synopsys is shifting from discrete IP licensing toward subsystems and eventually chiplets, reflecting customer demand for higher customization. Management is exploring new monetization models, including royalties, to capture more value.

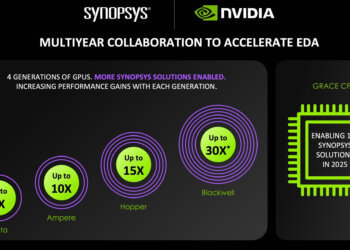

- AI and EDA Momentum – Roughly 20 customers are piloting Synopsys.ai GenAI capabilities. Hardware demand was strong, with record shipments of ZeBu Server 5 and HAPS 200 platforms, supporting complex AI chip design.

- Ansys Integration – Simulation and analysis solutions accounted for ~$78 million in Q3 revenue. Synopsys is embedding NVIDIA Omniverse into Ansys products and plans its first fully integrated Synopsys–Ansys solution in the first half of 2026.

- Financial Outlook – Backlog reached $10.1 billion, including Ansys. Management reiterated FY2025 revenue guidance of $7.03–$7.06 billion, but flagged continued IP headwinds into FY2026.

- Regional Trends – Europe and North America showed strength; China improved sequentially but remains under pressure.

- Efficiency Measures – Synopsys plans a ~10% global headcount reduction by FY2026 as part of its transformation, targeting higher growth areas while streamlining operations.

- Customer Concentration – Synopsys acknowledged outsized exposure to certain large customers but sees Ansys helping diversify across regions and industries.

- Debt and Cash – Ended Q3 with $2.6 billion cash and $14.3 billion debt. Management expects to begin paying down term loans in 2026; maturities fall in 2027–2028.

- Long-Term Margins – Despite near-term IP headwinds, Synopsys reaffirmed its commitment to mid-40% non-GAAP operating margins over the long term.