Smartphone sales figures from Q4 2017 are now mostly in and the reports confirm what many analysts suspected. The worldwide market for smartphones has stagnated and even begun to decline, perhaps because penetration rates in most countries have reached maximum levels, or perhaps because the replacement cycle is not nearly as fast as was once expected.

The smartphone sales trend is significant because it has been a leading predictor of bandwidth growth. Two years, if a mobile operator only had 25% of its subscribers using smartphones and enrolled in a 4G data plan, it was a sure bet that revenue and bandwidth growth would occur. Now, with most millennial customers packing a modern Android or iOS smartphone, it is not so certain that this growth will continue at the same pace. Bandwidth growth will come from usage and not simply millions of new smartphone users joining the network each month. This trend is playing out in the U.S., which reached 4G saturation much earlier, as well as China and India, which have been the big growth stories more recently.

Certainly, pricing for the flagship devices from Apple, Samsung, Google and LG has put off many consumers from upgrading their smartphones just on a whim. At the $900 to $1000 or more price range, device manufacturers are testing the limits of consumer budgets and many folks seem to be holding off.

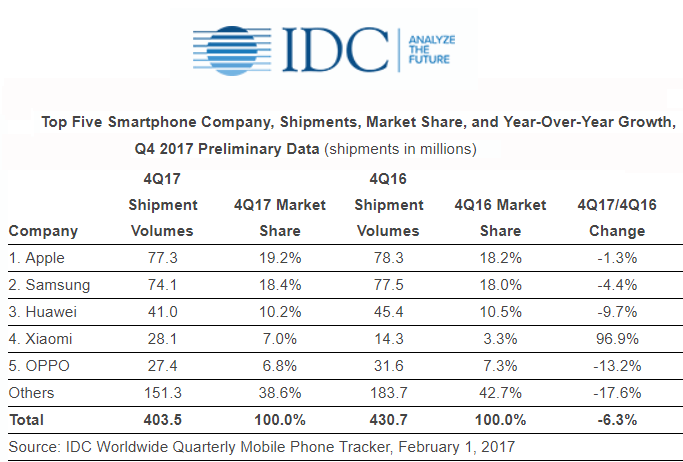

Preliminary data from the International Data Corporation (IDC) Worldwide Quarterly Mobile Phone Tracker indicates that indeed a contraction in the smartphone business occurred in 2017. IDC says smartphone vendors shipped a total of 403.5 million units during the fourth quarter of 2017 (4Q17), resulting in a 6.3% decline when compared to the 430.7 million units shipped in the final quarter of 2016. For the full year, the worldwide smartphone market saw a total of 1.472 billion units shipped, declining less than 1% from the 1.473 billion units shipped in 2016.

“In the presence of ultra-high-end flagships, the still high-priced flagships from the previous generation seemed far more palatable to consumers in 2017,” said Jitesh Ubrani, senior research analyst with IDC’s Worldwide Mobile Device Trackers. “Many high-profile companies offered their widest product portfolio ever in hopes of capturing a greater audience. Meanwhile, brands outside the top 5 struggled to maintain momentum as value brands such as Honor, Vivo, Xiaomi, and OPPO offered incredible competition at the low end, and brands like Apple, Samsung, and Huawei maintained their stronghold on the high end.”

IDC’s study also provides an update on the big brands:

Apple experienced a slight downturn from the previous holiday quarter as iPhone volumes reached 77.3 million units, a year-over-year decline of 1.3%. Although demand for the new higher priced iPhone X may not have been as strong as many expected, the overall iPhone lineup appealed to a wider range of consumers in both emerging and developed markets. Apple finished second for the full year in 2017 shipping 215.8 million units, up 0.2% from the 215.4 million units shipped in 2016.

Samsung remained the overall leader in the worldwide smartphone market for 2017 despite losing out to Apple in the fourth quarter. The Korean giant shipped 74.1 million units in 4Q17, down 4.4% compared to the 77.5 million units from last year. Samsung finished the year with 317.3 million shipments, up 1.9% from the 311.4 million shipments in 2016.

Huawei continues to hold the number three position despite intensified competition from growing Chinese players such as OPPO and Vivo. Huawei shipped 41.0 million units, down 9.7% from the 45.4 million shipped in the fourth quarter of 2016. The 2017 results look much better for the Chinese giant as the Honor brand helped pushed sales both inside and outside of China. Huawei shipped 153.1 million units, up 9.9% from the 139.3 million unit shipped in 2016. Recent aspirations for breaking into the U.S. market are on hold as both AT&T and Verizon recently cut ties to bring Huawei flagships to the U.S.

Xiaomi managed to double its share to 7% from 3.3% during the holiday quarter last year. This comes as no surprise since the company has continued to focus on growth outside China, with India and Russia being two of its largest markets. The company has been expanding its number of Mi Stores and Mi Service Centers, with fast buildout coming in markets like Indonesia. In India, Xiaomi also launched Redmi Y-series in India and roped in Bollywood celebrity Katrina Kaif to endorse the selfie-centric smartphone series as its first product endorser. The Redmi 5A, which was launched at US$78, saw more than a million devices being sold within a month.

OPPO dropped one place to the 5th position as the company shipped 27.4 million smartphones while managing to maintain 12% growth for the full year, amounting to 111.8 million smartphones. Like Xiaomi, OPPO has also managed to move beyond the domestic Chinese market and gain a foothold in other Asian countries like India, Indonesia, and Vietnam. In Indonesia, it launched the new F5 series in 4Q17 and also announced its partnership with AOV, a MOBA game.

A second research report, from Strategy Analytics, found that global smartphone shipments tumbled 9 percent annually to reach 400 million units in Q4 2017. Strategy Analytics crowns Apple with a first place finish at 19% global marketshare, nudging Samsung into second position. Xiaomi continued its relentless rise, almost doubling smartphone shipments from a year ago.

Linda Sui, Director at Strategy Analytics, said, “The shrinkage in global smartphone shipments was caused by a collapse in the huge China market, where demand fell 16 percent annually due to longer replacement rates, fewer operator subsidies and a general lack of wow models. However, on a full-year basis, global smartphone shipments grew 1 percent and topped an impressive 1.5 billion units for the first time ever.”

“OPPO shipped 29.5 million smartphones during Q4 2017, unmoved from 29.5 million units in Q4 2016. OPPO was growing smartphone shipments at a 99 percent annual rate a year ago, but its growth has now dropped to zero. The golden age for OPPO is coming to an end and it is facing serious competition from Xiaomi and others. Xiaomi soared 87 percent annually, taking fifth place with 27.8 million shipments, more than doubling its global smartphone marketshare to 7 percent in Q4 2017, up from 3 percent a year ago.”