Verizon raised its full-year 2025 guidance for adjusted EBITDA, earnings per share (EPS), and free cash flow following strong second-quarter results. The company posted $34.5 billion in revenue for Q2 2025, a 5.2% increase year-over-year, with net income rising to $5.1 billion from $4.7 billion a year earlier. Wireless service revenue grew 2.2% to $20.9 billion, while broadband net additions reached 293,000, including 278,000 fixed wireless access customers.

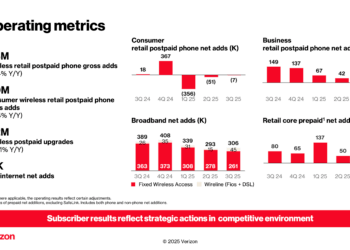

The Consumer segment posted $26.6 billion in revenue, up 6.9% from Q2 2024, with average revenue per account (ARPA) rising to $147.50. Consumer churn rates remained stable, with 51,000 postpaid phone net losses—an improvement from 109,000 in the prior year. On the Business side, operating income increased 27.6% year-over-year, despite a slight dip in revenue to $7.3 billion. Business added 65,000 retail postpaid connections, including 42,000 phones.

Based on its momentum and favorable tax reforms, Verizon now expects full-year adjusted EBITDA to grow 2.5%–3.5%, adjusted EPS to rise 1.0%–3.0%, and free cash flow to reach between $19.5 billion and $20.5 billion. Capital expenditures are projected to be $17.5–18.5 billion, excluding any impact from the pending Frontier acquisition.

- Q2 2025 revenue: $34.5B (+5.2% YoY); net income: $5.1B

- Wireless service revenue: $20.9B (+2.2% YoY); broadband net adds: 293,000

- Fixed wireless access subscribers exceed 5.1M; target 8–9M by 2028

- Consumer segment revenue: $26.6B (+6.9% YoY); ARPA: $147.50

- Business segment operating income up 27.6% YoY; EBITDA margin: 22.9%

- Updated 2025 guidance:

- Adjusted EBITDA growth: 2.5%–3.5%

- Adjusted EPS growth: 1.0%–3.0%

- Free cash flow: $19.5B–$20.5B

- CapEx: $17.5B–$18.5B

“Our unmatched and award-winning network combined with our financial strength enables us to continually innovate and enhance our products and services, empowering how people live, work and play,” said Hans Vestberg, Verizon Chairman and CEO.

🌐 Why it Matters: Verizon’s Q2 results signal a pivotal moment in the telecom industry’s transition toward fixed wireless access (FWA) as a major broadband alternative. With 278,000 net additions this quarter and a total base now exceeding 5.1 million subscribers, FWA has become a cornerstone of Verizon’s broadband growth strategy. Unlike traditional fiber deployments, FWA offers lower capital intensity and faster deployment timelines—critical advantages as the company targets 8–9 million FWA subscribers by 2028. This also reflects shifting customer expectations for simple, home-based broadband solutions that can ride on existing 5G infrastructure.

The 2.3% year-over-year increase in average revenue per account (ARPA) to $147.50 demonstrates that Verizon is succeeding in monetizing customer relationships through service bundling and segmentation. Plans like myPlan, Best Value Guarantee, and myHome encourage customers to add services such as streaming, device protection, and cloud storage—raising ARPA without relying on pure subscriber growth.

Importantly, Verizon’s improved financial outlook also reflects favorable tax provisions within the Infrastructure Investment and Jobs Act (the so-called “Big Beautiful Bill”). These include enhanced deductions for capital expenditures and accelerated depreciation for qualifying infrastructure investments—critical levers for companies investing heavily in network buildouts. For a capital-intensive operator like Verizon, these tax incentives improve after-tax returns on FWA, fiber, and 5G deployments. The result is a more favorable investment climate that enables large telcos to expand infrastructure while maintaining strong free cash flow and earnings growth.